: Laurent Doucet; Shrikant Bhat; Javier Lastra; Pauline Sim; Akhil Doegar; Dennis Liu.")

Asia insurers risk irrelevance as protection gaps widen

An expert said Singapore saves 36% of its income despite having high protection and critical illness gaps.

Asia's insurance industry is rethinking how it defines customer value as ageing populations, widening protection gaps and advances in artificial intelligence (AI) force insurers to move beyond selling policies toward delivering personalised financial and health solutions.

"Customers perceive value from a point of view of how well we are addressing their concerns, and longevity is probably one of the top concerns for customers today," Shrikant Bhat, CEO, AIA Group Unit-Linked and Pensions Business, AIA Group, told attendees of the Asian Banking & Finance and Insurance Asia Summit in Singapore on 1 July.

"The concern for customers is how they harness the longevity dividend. They obviously need financial assets that help them live a better lifestyle, they're obviously thinking about health plans, healthcare as they age, and whether the adequacy of that. That's where the value creation for customers is pretty high," Bhat added.

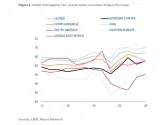

Panel moderator Laurent Doucet, Partner - Insurance Asia at Roland Berger, noted Singapore's old-age dependency ratio is expected to rise from about 20% today to around 40% by 2050, whilst Japan's ratio is projected to reach 75% and Hong Kong's could approach 100%.

This signals increasing pressure on insurers to develop products that address retirement adequacy, healthcare costs and wealth preservation.

Singapore continues to grapple with a sizeable protection gap despite strong household wealth. Akhil Doegar, Group Head of Distribution at Singlife, argued that insurers have focused too heavily on products rather than customer needs.

"Singapore is the world's highest GDP per capita, $65,555.06 (S$85,000). We have the highest savings rate in the world, 36% of what we earn is saved. At the same time, we are one of the countries with the highest protection gaps and the highest CI gap. If we are so rich, how come we are so underprotected?" Doegar said.

"The real need of a customer is not buying a product. What a customer needs from an insurance company is the ability to manage their cash flows at any stage of their life," Doegar added.

The Life Insurance Association, Singapore (LIA Singapore) reported that total weighted new business premiums reached $5.2b (S$6.53b) for the full year, up 11.3% from 2024.

Growth was mainly driven by higher annual premium sales. In the fourth quarter alone, new business premiums rose 13.0% compared to the same period a year earlier.

Investment-linked products (ILPs) made up the largest share of new business for Singapore’s life insurance industry in 2025, accounting for 44% of total weighted new business premiums.

Panellists agreed that AI will play an increasingly important role, but not as a replacement for advisers.

Javier Lastra, CEO of Swiss Life (Singapore) Pte Ltd, said the industry's competitive advantage remains personalised advice.

"The future is more human advice enriched by artificial intelligence," Lastra said. "The most valuable asset is trust. clients get virtually naked in front of us because they are going to share with us not only personal but also sensitive information,"

Pauline Sim, Head of Strategy & Transformation Office and Acting Head of Bancassurance, Commercial Distribution Division at United Overseas Insurance Limited, said insurers also face operational trade-offs when designing customer-centric experiences.

"Customer centricity often. will conflict with the process or the ideal product or information that we need internally," Sim said.

"Whenever we think about customer centricity, we're trying to balance between centricity and security. You also want to give customers the trust that whatever services we deliver, and whatever information they share with us, it is secure," Sim added.

Dennis Liu, Chief Technology Officer of Etiqa Insurance & Takaful, said fragmented customer information remains one of the industry's biggest obstacles.

"We have a lot of data everywhere, but the very challenge is we don't use data effectively," Liu said. "We want to use our data, we want to centralise data. Then we can offer the things we believe can deliver value to customers," Liu added that lowering operating costs through automation would enable insurers to return more value to policyholders.

Etiqa has already introduced AI-enabled services such as automated travel delay claims, proactive outreach following fire incidents and crash detection that initiates claims support without waiting for customers to report accidents.

Looking ahead, executives said insurers that align products with long-term customer outcomes rather than short-term sales metrics will be better positioned.

Bhat said AIA increasingly focuses on retirement income, wealth transfer and customer outcomes instead of product complexity.

"We deliver outcomes. We don't focus so much on how we do it," he said, adding that technology will help simplify products for both advisers and customers.

Doegar added that insurers should remain focused on closing Singapore's protection and retirement gaps rather than pursuing short-term gains.

"We have one job to close the protection and retirement gap in Singapore. If we stick to that path. " We will naturally grow by doing the right thing," Doegar said.

Advertise

Advertise